Chapter 5 Risk Prediction and Validation (Part I)

5.1 Risk Prediction/Stratification

For binary outcomes, a risk prediction is related to the predicted probability that an individual has or will develop a certain condition/trait.

Examples of a risk prediction for a binary outcome:

Probability that someone has hypertension.

Probability that someone has type-2 diabetes.

Probability someone will be hospitalized over the next 1 year.

Risk stratification: Often, a risk prediction model will only report whether or not someone belongs to one of several risk strata.

- For example, high, medium, or low risk.

5.2 Area under the ROC curve and the C-statistic

5.2.1 Sensitivity and Specificity

Let \(g(\mathbf{x}_{i})\) be a risk score for an individual with covariate vector \(\mathbf{x}_{i}\).

Higher values of \(g(\mathbf{x}_{i})\) are supposed to imply greater probability that the binary outcome \(Y_{i}\) is equal to \(1\).

- Though \(g(\mathbf{x}_{i})\) does not necessarily have to be a predicted probability.

The value \(t\) will be a threshold which determines whether or not, we predict \(Y_{i} = 1\) or not.

- \(g(\mathbf{x}_{i}) \geq t\) implies \(Y_{i} = 1\)

- \(g(\mathbf{x}_{i}) < t\) implies \(Y_{i} = 0\)

The sensitivity of the risk score \(g(\mathbf{x}_{i})\) with the threshold \(t\) is defined as the probability you “predict” \(Y_{i} = 1\) assuming that \(Y_{i}\) is, in fact, equal to \(1\).

In other words, the sensitivity is the probability of making the right decision given that \(Y_{i} = 1\).

- Sensitivity is often called the “true positive rate”.

The sensitivity is defined as: \[\begin{eqnarray} \textrm{Sensitivity}(t; g) &=& P\big\{ g(\mathbf{x}_{i}) \geq t| Y_{i} = 1 \big\} \nonumber \\ &=& \frac{P\big\{ g(\mathbf{x}_{i}) \geq t, Y_{i} = 1 \big\}}{P\big\{ Y_{i} = 1 \big\} }\nonumber \\ &=& \frac{P\big\{ g(\mathbf{x}_{i}) \geq t, Y_{i} = 1 \big\}}{ P\big\{ g(\mathbf{x}_{i}) \geq t, Y_{i} = 1 \big\} + P\big\{ g(\mathbf{x}_{i}) < t, Y_{i} = 1 \big\}} \end{eqnarray}\]

For a worthless risk score that is totally uninformative about the outcome, we should expect the sensitivity to be close to \(P\{ g(\mathbf{x}_{i}) \geq t \}\).

- You can compute the in-sample sensitivity with \[\begin{eqnarray} \hat{\textrm{Sensitivity}}(t; g) &=& \frac{\sum_{i=1}^{n} I\big\{ g(\mathbf{x}_{i}) \geq t, Y_{i} = 1 \big\} }{ \sum_{i=1}^{n} I\big\{g(\mathbf{x}_{i}) \geq t, Y_{i} = 1 \big\} + \sum_{i=1}^{n} I\big\{ g(\mathbf{x}_{i}) < t, Y_{i} = 1 \big\}} \nonumber \\ &=& \frac{\textrm{number of true positives}}{\textrm{number of true positives} + \textrm{number of false negatives} } \end{eqnarray}\]

The specificity of the risk score \(g(\mathbf{x}_{i})\) with the threshold \(t\) is defined as the probability you “predict” \(Y_{i} = 0\) assuming that \(Y_{i}\) is, in fact, equal to \(0\).

The specificity is defined as: \[\begin{eqnarray} \textrm{Specificity}(t; g) &=& P\big\{ g(\mathbf{x}_{i}) < t| Y_{i} = 0 \big\} \nonumber \\ &=& \frac{P\big\{ g(\mathbf{x}_{i}) < t, Y_{i} = 0 \big\}}{ P\big\{ g(\mathbf{x}_{i}) < t, Y_{i} = 0 \big\} + P\big\{ g(\mathbf{x}_{i}) \geq t, Y_{i} = 0 \big\}} \end{eqnarray}\]

Note that \(1 - \textrm{Specificity}(t; g) = P\big\{ g(\mathbf{x}_{i}) \geq t| Y_{i} = 0 \big\}\).

- \(1 - \textrm{Specificity}(t; g)\) is often called the “false positive rate”

You can compute the in-sample specificity with \[\begin{eqnarray} \hat{\textrm{Specificity}}(t; g) &=& \frac{\sum_{i=1}^{n} I\big\{ g(\mathbf{x}_{i}) < t, Y_{i} = 0 \big\} }{ \sum_{i=1}^{n} I\big\{g(\mathbf{x}_{i}) < t, Y_{i} = 0 \big\} + \sum_{i=1}^{n} I\big\{ g(\mathbf{x}_{i}) \geq t, Y_{i} = 0 \big\}} \nonumber \\ &=& \frac{\textrm{number of true negatives}}{\textrm{number of true negatives} + \textrm{number of false positives} } \end{eqnarray}\]

For a worthless risk score that is totally uninformative about the outcome, we should expect the specificity to be close to \(P\{ g(\mathbf{x}_{i}) < t \}\).

Note that high values of both sensitivity and specificity is good.

- For a “perfect” risk score, both sensitivity and specificity would be equal to \(1\).

5.2.2 The ROC curve

The receiver operating characteristic (ROC) curve graphically depicts how sensitivity and specificity change as the threshold \(t\) varies.

Let \(t_{i} = g(\mathbf{x}_{i})\) and let \(t_{(1)} > t_{(2)} > ... > t_{(n)}\) be the ordered values of \(t_{1}, \ldots, t_{n}\).

To construct an ROC curve we are going to plot sentivity vs. 1 - specificity for each of the thresholds \(t_{(1)}, \ldots, t_{(n)}\).

Let \(x_{i} = 1 - \hat{\textrm{Specificity}}(t_{(i)}; g)\) and \(y_{i} = \hat{\textrm{Sensitivity}}(t_{(i)}; g)\).

We will define \(x_{0} = y_{0} = 0\) and \(x_{n+1} = y_{n+1} = 1\).

- \(x_{0}\), \(y_{0}\) represent 1 - specificity and sensitivity when using \(t = \infty\).

- \(x_{n+1}\), \(y_{n+1}\) represent 1 - specificity and sensitivity when using \(t = -\infty\).

Plotting \(y_{i}\) vs. \(x_{i}\) for \(i = 0, \ldots, n+1\) will give you the ROC curve.

Ideally, the values of \(y_{i}\) will close to \(1\) for all \(i\).

For a worthless risk score we should expect both \(y_{i}\) and \(x_{i}\) to be roughly equal to \(P(g(\mathbf{x}_{i}) \geq t)\).

Hence, plotting \(y_{i}\) vs. \(x_{i}\) should be fairly close to the line \(y=x\).

5.2.3 Computing the ROC curve

- To try computing an ROC curve, we will use the Wisconsin Breast Cancer dataset

which is available in the

biopsydataset from theMASSpackage.

## ID V1 V2 V3 V4 V5 V6 V7 V8 V9 class

## 1 1000025 5 1 1 1 2 1 3 1 1 benign

## 2 1002945 5 4 4 5 7 10 3 2 1 benign

## 3 1015425 3 1 1 1 2 2 3 1 1 benign

## 4 1016277 6 8 8 1 3 4 3 7 1 benign

## 5 1017023 4 1 1 3 2 1 3 1 1 benign

## 6 1017122 8 10 10 8 7 10 9 7 1 malignant##

## benign malignant

## 458 241##

## 0 1

## 458 241Let’s compute risk scores for tumor malignancy by using a logistic regression model with

classas the outcome and variablesV1, V3, V4, V7, V8as the covariates.Our risk score for the \(i^{th}\) case, will be the predicted probability of having a malignant tumor given the covariate information

logreg.model <- glm(tumor.type ~ V1 + V3 + V4 + V7 + V8, family="binomial", data=biopsy)

risk.score <- logreg.model$fitted.values- Let’s now compute the sensitivity and specificity for a threshold of \(t = 0.5\)

Sensitivity <- function(thresh, Y, risk.score) {

sum((risk.score >= thresh)*Y)/sum(Y)

}

Specificity <- function(thresh, Y, risk.score) {

sum((risk.score < thresh)*(1 - Y))/sum(1 - Y)

}

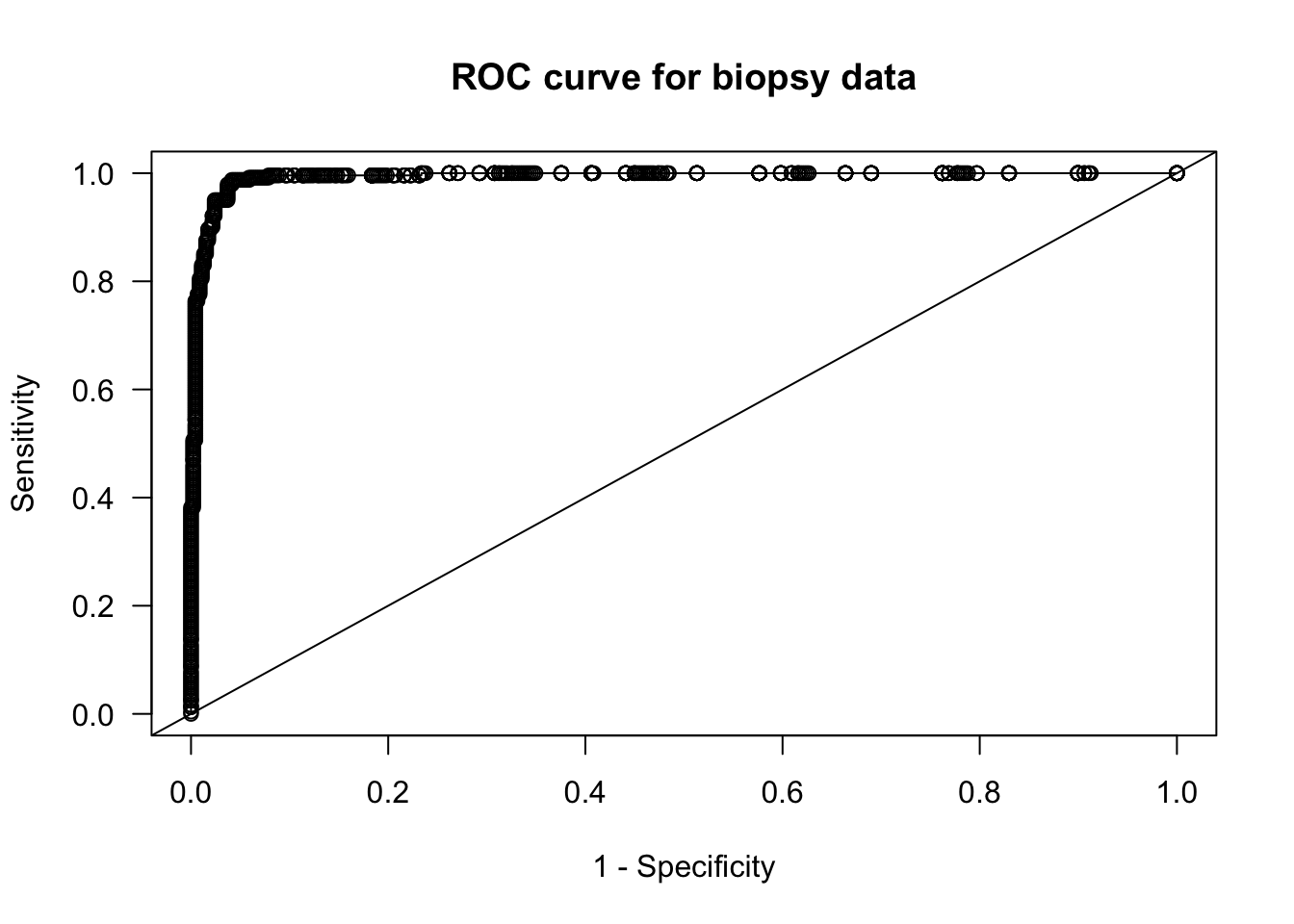

Sensitivity(0.5, Y=biopsy$tumor.type, risk.score)## [1] 0.9502075## [1] 0.9759825- For the threshold of \(t = 0.5\), we have a sensitivity of about \(0.95\) and a specificity of about \(0.975\).

- Now, let’s compute the ROC curve by computing sensitivity and specificity for each risk score (plus the values of 0 and 1).

sorted.riskscores <- c(1, sort(risk.score, decreasing=TRUE), 0)

mm <- length(sorted.riskscores)

roc.y <- roc.x <- rep(0, mm)

for(k in 1:mm) {

thresh.val <- sorted.riskscores[k]

roc.y[k] <- Sensitivity(thresh.val, Y=biopsy$tumor.type, risk.score)

roc.x[k] <- 1 - Specificity(thresh.val, Y=biopsy$tumor.type, risk.score)

}

plot(roc.x, roc.y, main="ROC curve for biopsy data", xlab="1 - Specificity",

ylab="Sensitivity", las=1)

lines(roc.x, roc.y, type="s")

abline(0, 1)

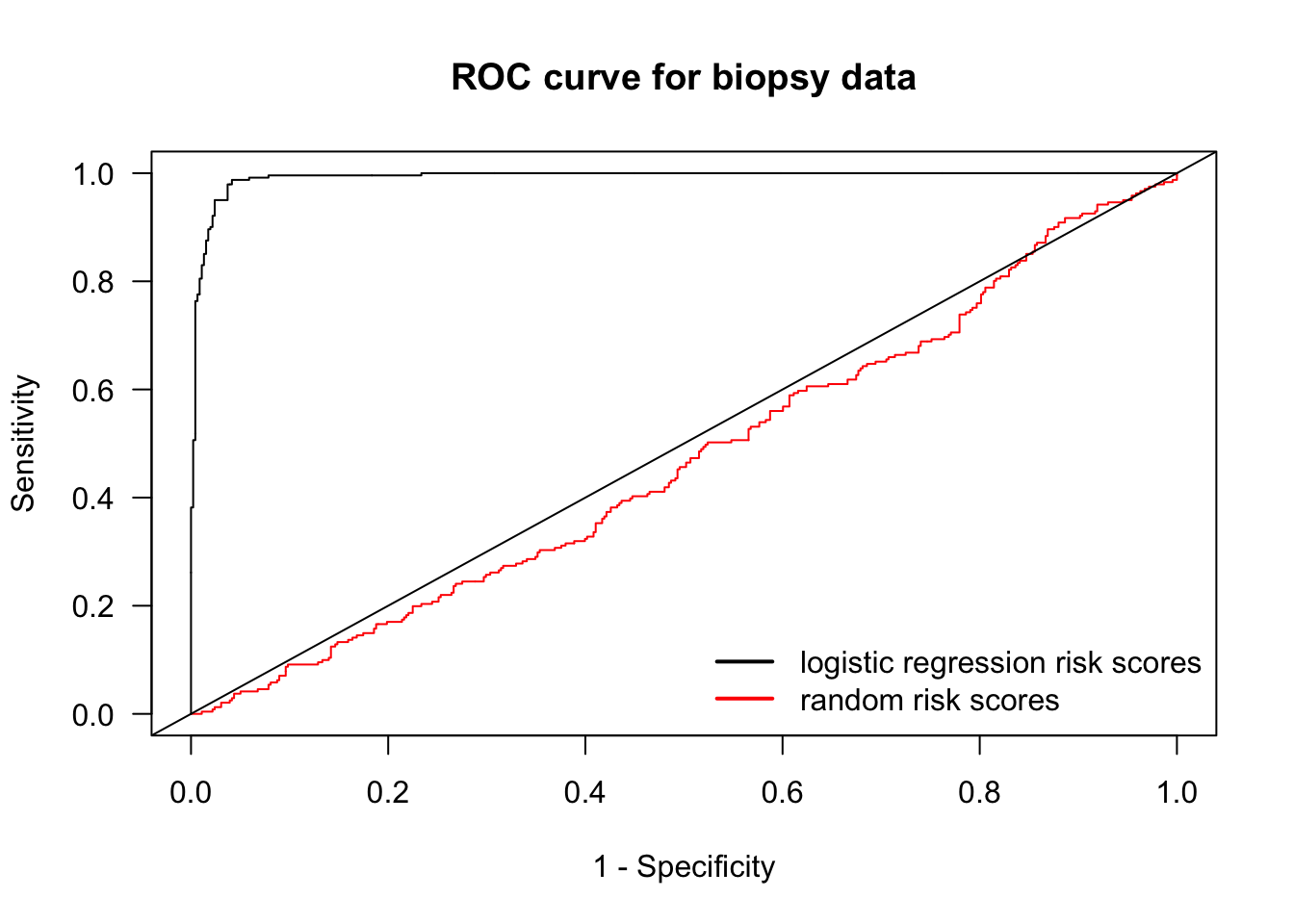

- Let’s compare the logistic regression ROC curve with a worthless risk score where we generate risk scores randomly from a uniform distribution.

rr <- runif(nrow(biopsy))

sorted.rr <- c(1, sort(rr, decreasing=TRUE), 0)

mm <- length(sorted.rr)

roc.random.y <- roc.random.x <- rep(0, mm)

for(k in 1:mm) {

thresh.val <- sorted.rr[k]

roc.random.y[k] <- Sensitivity(thresh.val, Y=biopsy$tumor.type, rr)

roc.random.x[k] <- 1 - Specificity(thresh.val, Y=biopsy$tumor.type, rr)

}

plot(roc.random.x, roc.random.y, main="ROC curve for biopsy data", xlab="1 - Specificity",

ylab="Sensitivity", las=1, col="red", type="n")

lines(roc.random.x, roc.random.y, type="s", col="red")

lines(roc.x, roc.y, type="s")

legend("bottomright", legend=c("logistic regression risk scores", "random risk scores"),

col=c("black", "red"), lwd=2, bty='n')

abline(0, 1)

5.3 Area under the ROC curve and the C-statistic

The Area Under the ROC curve AUC is the area under the graph of the points \((x_{i}, y_{i})\), \(i = 0, \ldots, n+1\).

The AUC is given by \[\begin{equation} AUC = \sum_{i=0}^{n} y_{i}(x_{i+1} - x_{i}) \end{equation}\]

5.3.1 Rewriting the formula for the AUC

Note that \[\begin{equation} y_{i} = \sum_{k=1}^{n} I\{ g(\mathbf{x}_{k}) \geq t_{(i)}\} I\{ Y_{k} = 1 \}\Big/\sum_{k=1}^{n} I\{ Y_{k} = 1\} = \frac{1}{n\hat{p}}\sum_{k=1}^{n} a_{ki}, \end{equation}\] where \(n\hat{p} = \sum_{k=1}^{n} I\{ Y_{k} = 1\}\) and \(a_{ki} = I\{ g(\mathbf{x}_{k}) \geq t_{(i)}\} I\{ Y_{k} = 1 \}\).

Because \(t_{(i)} \geq t_{(i+1)}\): \[\begin{eqnarray} x_{i+1} - x_{i} &=& \sum_{k=1}^{n} \Big(I\{ g(\mathbf{x}_{k}) \geq t_{(i+1)}, Y_{k} = 0 \} - I\{ g(\mathbf{x}_{k}) \geq t_{(i)}, Y_{k} = 0 \}\Big)\Big/\sum_{k=1}^{n} I\{ Y_{k} = 0\} \nonumber \\ &=& \frac{1}{n(1 - \hat{p})}\sum_{k=1}^{n} I\{g(\mathbf{x}_{k}) < t_{(i)}\} I\{ g(\mathbf{x}_{k}) \geq t_{(i+1)}\} I\{Y_{k} = 0 \} \\ &=& \frac{1}{n(1 - \hat{p})}\sum_{k=1}^{n} I\{ g(\mathbf{x}_{k}) = t_{(i+1)}\} I\{Y_{k} = 0 \} \nonumber \\ &=& \frac{1}{n(1 - \hat{p})}\sum_{k=1}^{n} b_{ki} \end{eqnarray}\] where \(n(1 - \hat{p}) = \sum_{k=1}^{n} I\{ Y_{k} = 0\}\) and \(b_{ki} = I\{ g(\mathbf{x}_{k}) = t_{(i+1)}\} I\{Y_{k} = 0 \}\).

So, we can express the AUC as: \[\begin{eqnarray} AUC &=& \frac{1}{n^{2}\hat{p}(1 - \hat{p})}\sum_{i=0}^{n} \sum_{k=0}^{n} a_{ki} \sum_{k=0}^{n} b_{ki} = \frac{1}{n^{2}\hat{p}(1 - \hat{p})} \sum_{k=0}^{n} \sum_{j=0}^{n}\sum_{i=0}^{n} a_{ki} b_{ji} \\ &=& \frac{1}{n^{2}\hat{p}(1 - \hat{p})} \sum_{k=0}^{n} \sum_{j=0}^{n} I\{ Y_{k} = 1 \} I\{Y_{j} = 0 \} \sum_{i=0}^{n} I\{ g(\mathbf{x}_{k}) \geq t_{(i)}\}I\{ g(\mathbf{x}_{j}) = t_{(i+1)}\} \tag{5.1} \end{eqnarray}\]

Note now that because the \(t_{(i)}\) are the ordered values of the \(g(\mathbf{x}_{h})\) \[\begin{equation} \sum_{i=0}^{n} I\{ g(\mathbf{x}_{k}) \geq t_{(i)}\}I\{ g(\mathbf{x}_{j}) = t_{(i+1)}\} = I\{ g(\mathbf{x}_{k}) \geq t_{(j^{*} - 1)}\} = I\{ g(\mathbf{x}_{k}) > t_{(j^{*})}\}, \end{equation}\] where \(j^{*}\) is the index such that \(t_{(j^{*})} = g(\mathbf{x}_{j})\).

Hence, \[\begin{equation} \sum_{i=0}^{n} I\{ g(\mathbf{x}_{k}) \geq t_{(i)}\}I\{ g(\mathbf{x}_{j}) = t_{(i+1)}\} = I\{ g(\mathbf{x}_{k}) > g(\mathbf{x}_{j}) \} \tag{5.2} \end{equation}\]

5.3.2 Interpreting the AUC

We can write the AUC as \[\begin{equation} \textrm{AUC} = S_{1}/S_{2} \end{equation}\]

The sum \(S_{2}\) counts the number of all discordant pairs of responses

- The pair of outcomes \((Y_{k}, Y_{j})\) is discordant if \(Y_{k} = 1\) and \(Y_{j}=0\) or vice versa. \[\begin{equation} S_{2} = \sum_{i=1}^{n}I\{ Y_{i} = 0\}\sum_{i=1}^{n} I\{Y_{i} = 1\} = \sum_{j=1}^{n}\sum_{k=1}^{n} I\{ Y_{j} = 0\} I\{Y_{k} = 1\} \end{equation}\]

Now, look at the sum \(S_{1}\): \[\begin{eqnarray} S_{1} &=& \sum_{k=0}^{n} \sum_{j=0}^{n} I\{ g(\mathbf{x}_{k}) > g(\mathbf{x}_{j}) \}I\{ Y_{k} = 1 \} I\{Y_{j} = 0 \} \end{eqnarray}\]

\(S_{1}\) looks at all discordant pairs of responses and counts the number of pairs where the risk score ordering agrees with the ordering of the responses.

To summarize: The AUC is the proportion of discordant outcome pairs where the risk score ordering for that pair agrees with the ordering of the outcomes

An AUC of \(0.5\) means that the risk score is performing about the same as a risk score generated at random.

The AUC is often referred to as the concordance index, or c-index.

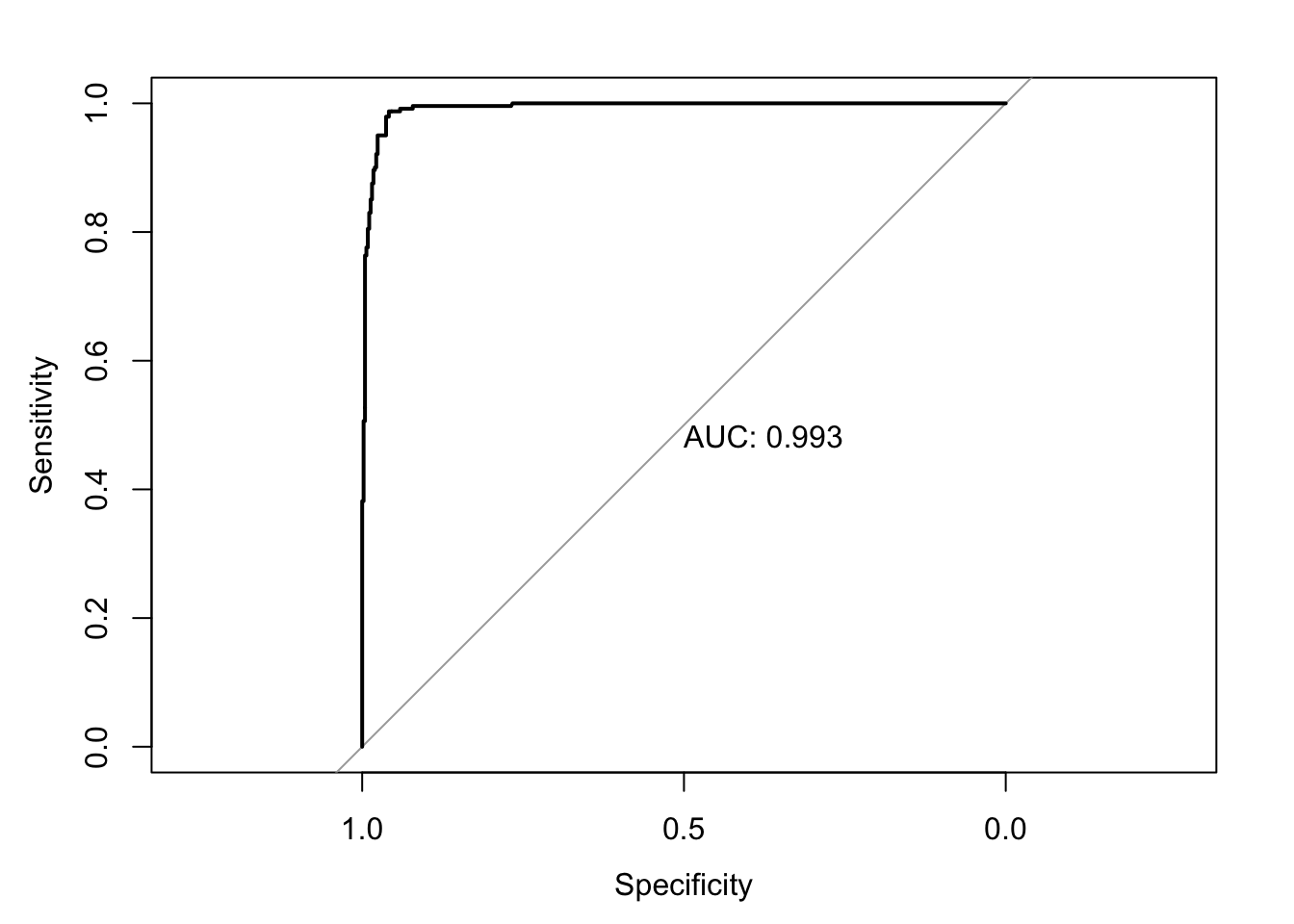

- Let’s compute the AUC for our logistic regression-based risk score for the

biopsydata:

## [1] 0.9928- This is a very high AUC: \(0.9928\)

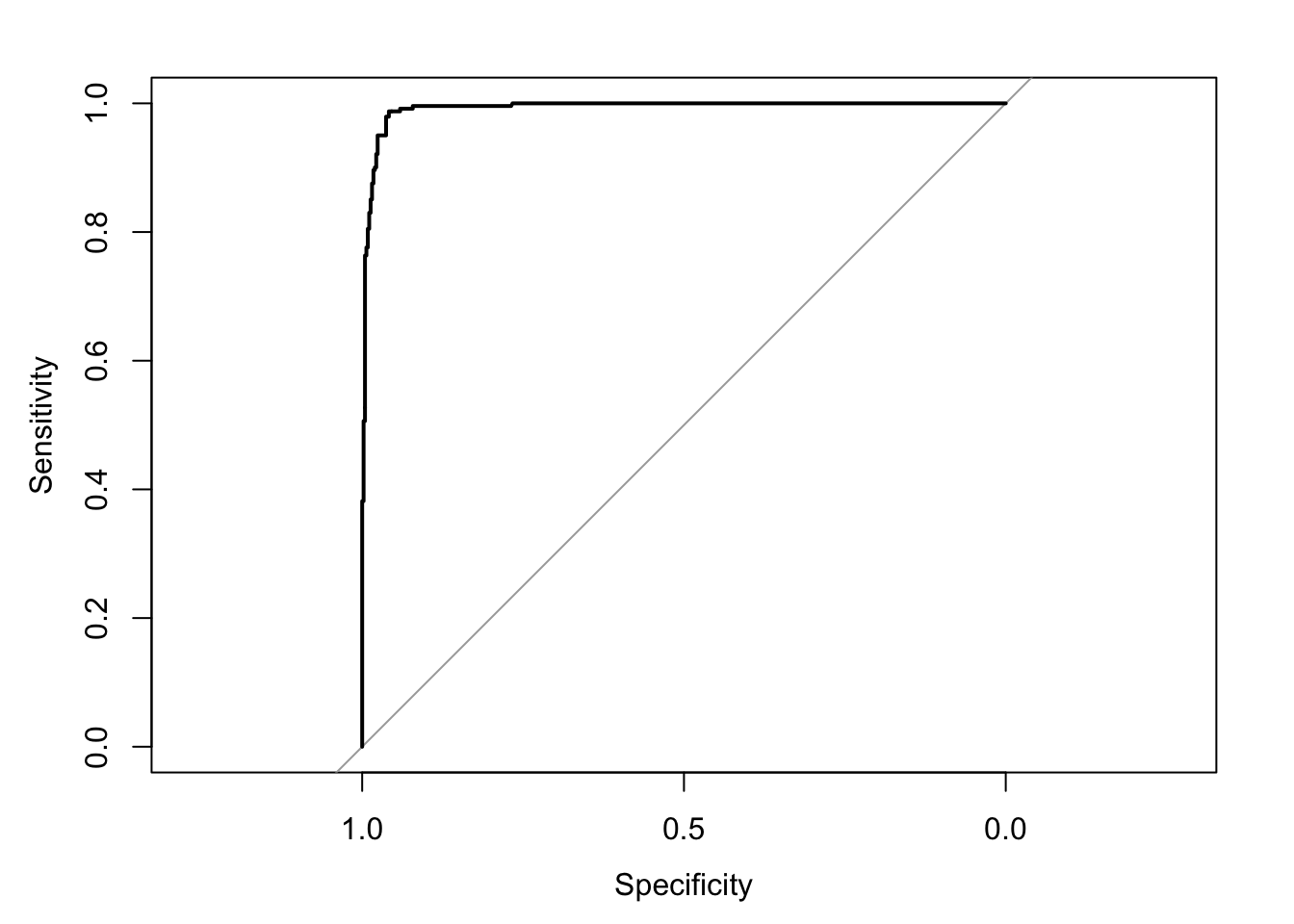

5.3.3 Computing the AUC in R

You can compute the AUC in R without writing all your own functions by using the

pROCpackage.With the

pROCpackage, you start by inputting your binary outcomes and risk scores into therocfunction in order to get an “roc object”.

- To find the AUC, you can then use

auc(roc.biopsy)

## Area under the curve: 0.9928- You can plot the ROC curve by just plugging in the roc object into the

plotfunction.

- To also print the AUC value, you can just add

print.auc=TRUE

5.4 Model Calibration

The AUC, or c-index is a measure of the statistical discrimination of the risk score.

However, a high value of the AUC does not imply that the risk score is well-calibrated.

Calibration refers to the agreement between observed frequency of the outcome and the fitted probabilities of those outcomes.

For example, if we look at a group of individuals all of whom have a fitted probability of \(0.2\), then we should expect that roughly \(20\%\) of the outcomes should equal \(1\) from this group.

We can examine this graphically by looking at the observed proportion of successes vs. the fitted probabilities for several risk strata.

Specifically, if we have risk score-cutoffs \(r_{1}, \ldots, r_{G}\), the observed proportion of successes in the \(k^{th}\) risk stratum is \[\begin{equation} O_{k} = \sum_{i=1}^{n} Y_{i}I\{ r_{k-1} < g(\mathbf{x}_{i}) \leq r_{k} \} \Big/\sum_{i=1}^{n} I\{ r_{k-1} < g(\mathbf{x}_{i}) \leq r_{k} \} \end{equation}\]

The expected proportion of successes in the \(k^{th}\) risk stratum is \[\begin{equation} P_{k} = \sum_{i=1}^{n} g(\mathbf{x}_{i})I\{ r_{k-1} < g(\mathbf{x}_{i}) \leq r_{k} \} \Big/\sum_{i=1}^{n} I\{ r_{k-1} < g(\mathbf{x}_{i}) \leq r_{k} \} \end{equation}\]

If \(g(\mathbf{x}_{i})\) is well-calibrated, \(O_{k}\) and \(P_{k}\) should be fairly similar for each \(k\).

Let’s make a calibration plot for the

biopsydata.First, let’s make 10 risk strata using the quantiles of our logistic regression-based risk score.

## 10% 20% 30% 40% 50%

## 0.000000000 0.001505966 0.002756161 0.005385182 0.010154320 0.019231612

## 60% 70% 80% 90%

## 0.074574998 0.841857858 0.989561027 0.999471042 1.000000000- Now, compute observed and expected frequencies for each of the risk strata and plot the result:

observed.freq <- pred.freq <- rep(0, 10)

for(k in 2:11) {

ind <- risk.score <= rr[k] & risk.score > rr[k-1] # stratum indicators

observed.freq[k] <- sum(biopsy$tumor.type[ind])/sum(ind)

pred.freq[k] <- sum(risk.score[ind])/sum(ind)

}

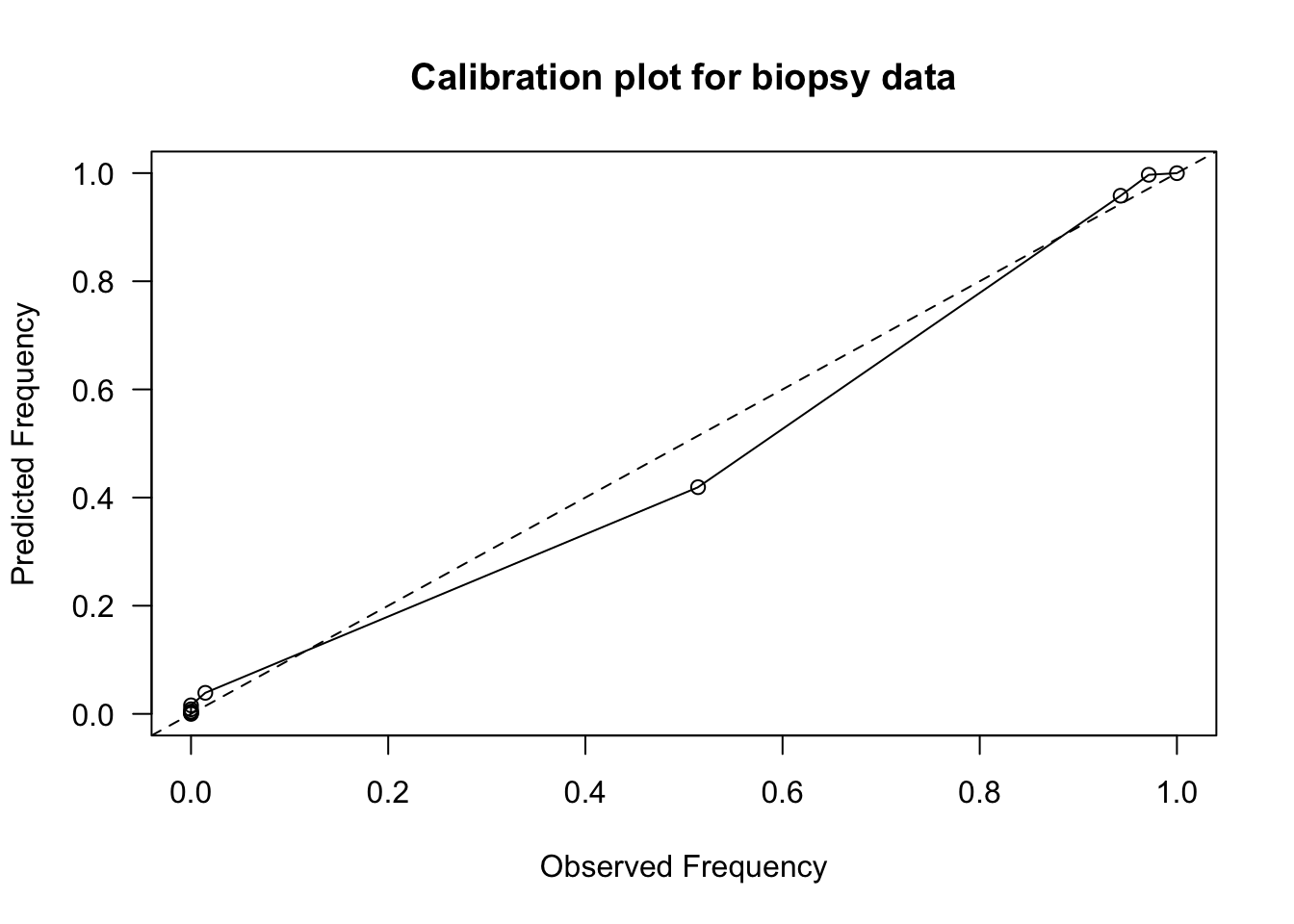

plot(observed.freq, pred.freq, xlab="Observed Frequency",

ylab = "Predicted Frequency",

las=1, main="Calibration plot for biopsy data")

lines(observed.freq, pred.freq)

abline(0, 1, lty=2)

- Most of the risk scores are more concentrated near zero, but this calibration plot shows fairly

good calibration.

- Expected vs. Observed frequencies are mostly close to the \(y = x\) straight line.

- Sometimes an estimated intercept and slope from

a regression of expected vs. observed frequencies is reported.

- We should expect that the intercept should be close to \(0\) and the slope should be close to \(1\) for a well-calibrated risk score.

##

## Call:

## lm(formula = pred.freq ~ observed.freq)

##

## Coefficients:

## (Intercept) observed.freq

## 0.001759 0.994948- The Hosmer–Lemeshow test is a more formal test that compares these types of observed vs. expected frequencies.

5.5 AUC and C-statistic for Survival Outcomes

In survival analysis, we have random variables \(T_{1}, \ldots, T_{n}\) which represent times until

Due to right-censoring, we only observe pairs: \((U_i, \delta_i)\), where

- \(U_i = \min(T_{i}, C_{i})\) is the last follow-up time

- \(\delta_i = I(T_{i} \leq C_{i})\) is the event indicator

- \(C_{i}\) - censoring time

The AUC for binary outcomes cannot directly be applied to survival outcomes.

With survival outcomes, we cannot directly separate outcomes into “events” vs. “no events”.

This is true even if we try to create a binary outcome: (survival past 5 years vs. not)

- For example, if Patient A is censored at \(t=4\) and Patient B has an event at \(t=10\), we cannot determine if Patient A survived past 5 years.

The standard C-statistic for survival data is an overall measure that quantifies how well a model predicts the ordering of survival times.

The C-statistics need to account for censoring.

5.5.1 What is the C-statistic for survival measuring?

Suppose we have a risk model \(g(\mathbf{x}_{i})\), that takes input covariate vectors \(\mathbf{x}_{i}\) and outpute a risk score.

- Higher values of the risk score should imply worse survival.

The underlying parameter that the C-statistic is trying to estimate is: \[\begin{equation} \theta_{C} = P\Big\{ g(\mathbf{x}_{i}) > g(\mathbf{x}_{j}) \Big| T_{j} > T_{i} \Big\} \end{equation}\]

A truncated version of \(\theta_{C}\) is often estimated: \[\begin{equation} \theta_{C, \tau} = P\Big\{ g(\mathbf{x}_{i}) > g(\mathbf{x}_{j}) \Big| T_{j} > T_{i}, T_{i} \leq \tau \Big\} \end{equation}\]

A truncated version is often used, because estimating \(\theta_{C}\) is often unstable if one considers values of \(T_{i}\) near the tail of the distribution.

5.5.2 Harrell’s C-Index

Harrell’s C is a well-known estimate of the C-statistic parameter \(\theta_{C}\).

- This is the default in the

glmnetpackage

- This is the default in the

Harrell’s C only looks at pairs of “evaluable” subjects.

- A pair of subjects \((i, j)\) is evaluable if we can definitively say who survived longer.

The pair \((i, j)\) is evaluable if:

- Both \(i\) and \(j\) have events (i.e., both \(i\) and \(j\) were not censored) OR

- One subject is censored after the other had an event (i.e., \(T_i < C_j\) or \(T_{j} < C_{i}\)).

The formula for Harrell’s C is then \[\begin{align} C_{\textrm{Harrell}} &= \frac{\sum_{i \ne j} I(\text{Pair is Evaluable}) \times I(\text{Concordant})}{\sum_{i \ne j} I(\text{Pair is Evaluable})} \nonumber \\ &= \frac{\sum_{i \ne j} \delta_{i} I(U_{i} < U_{j}) I\big(g(\mathbf{x}_{i}) > g(\mathbf{x}_{j}) \big)}{\sum_{i \ne j} \delta_{i} I(U_{i} < U_{j})}. \nonumber \end{align}\]

Concordant: The subject with shorter survival time had higher predicted risk.

Discordant: The subject with shorter survival time had lower predicted risk.

- While widely used, Harrell’s C has a number of limitations

Censoring Distribution Dependence: Harrell’s C depends on the study-specific censoring distribution. If two studies have the same underlying survival distributions for the outcome of interest but different censoring patterns, they will report different C-statistics.

Bias with Heavy Censoring: It systematically overestimates performance as censoring increases. This is because it discards pairs where the shorter time is censored.

5.5.3 Uno’s C-Statistic (Inverse Probability Weighting)

Uno’s C-statistic is an adjustment of Harrell’s C that uses Inverse Probability of Censoring Weights (IPCW).

Instead of treating all evaluable pairs equally, Uno’s C weights pairs by the probability that they were observed (not censored).

Uno’s C-statistic still considers only evaluable pairs, but weights them: \[\begin{equation} C_{Uno} = \frac{\sum_{i,j} \{ \hat{G}(U_{i})\}^{-2} \delta_i I(U_{i} < U_{j}, U_{i} < \tau) I( g(\mathbf{x}_{i} ) > g(\mathbf{x}_{j})) }{\sum_{i,j} \{ \hat{G}(U_{i})\}^{-2} \Delta_i I(U_i < U_j) } \end{equation}\]

\(\hat{G}(t)\) estimate of the censoring survival distribution \(G(t) = P(C_{i} > t)\).

Uno’s C is consistent for the true concordance probability regardless of the censoring distribution (assuming independent censoring).

5.5.4 Survival C-statistics in R

The

concordancemethod from thesurvivalpackage can compute Harrell’s C-statistic from a Cox model.The risk score from a Cox model is: \[\begin{equation} g(\mathbf{x}_{i}) = \sum_{j=1}^{p} \hat{\beta}_{j}x_{ij} \nonumber \end{equation}\]

Let’s look at Harrell’s C-statistic for a Cox model with covariates

ageandsexfrom thelungdata

library(survival)

library(survC1) # For Uno's C

fit1 <- coxph(Surv(time, status) ~ age + sex, data = lung)

concordance(fit1)## Call:

## concordance.coxph(object = fit1)

##

## n= 228

## Concordance= 0.6029 se= 0.0255

## concordant discordant tied.x tied.y tied.xy

## 11910 7793 311 28 0With just

ageandsex, we have a C-statistic of 0.602Let’s look at the C-statistic when we add

ph.ecogandph.karno

## Call:

## concordance.coxph(object = fit2)

##

## n= 226

## Concordance= 0.6317 se= 0.02497

## concordant discordant tied.x tied.y tied.xy

## 12335 7184 43 28 0- Compare with Uno’s C-statistic

- This can be done by including the

timewt = "n/G2"argument

- This can be done by including the

## Call:

## concordance.coxph(object = fit2, timewt = "n/G2")

##

## n= 226

## Concordance= 0.6233 se= 0.02315

## concordant discordant tied.x tied.y tied.xy

## 15730.74 9495.97 55.47 35.24 0.005.6 Longitudinal Data and Risk Score Validation

When you have longitudinal responses \(Y_{ij}\), sensitivity, specificity, and the AUC/c-index will depend on what exactly you are trying to predict.

If you are trying to predict \(Y_{ij} = 1\) vs. \(Y_{ij} = 0\) for each \(j\), sensitivity and specificity will be defined by \[\begin{equation} P\{ g(\mathbf{x}_{ij}) \geq t|Y_{ij} = 1\} \qquad \textrm{ and } \qquad P\{ g(\mathbf{x}_{ij}) < t|Y_{ij} = 0\} \end{equation}\]

Here, \(g(\mathbf{x}_{ij})\) would be a risk score based on covariate information up to and including time \(t_{ij}\) and could include responses before time \(t_{ij}\).

In this case, the AUC would be calculated in the same way as the non-longitudinal case - you would just sum over all responses and risk scores across all individuals and time points.

In other cases, you may want to predict a single outcome \(\tilde{Y}_{i}\) even though the covariates are collected longitudinally over additional time points.

For example, \(\tilde{Y}_{i}\) might be an indicator of whether or not a patient is hypertensive over a particular time window.

In this case, you might compute a single risk score \(\hat{g}_{i}\) for each individual.

For example, \(\hat{g}_{i} = \frac{1}{n_{i}}\sum_{j=1}^{n_{i}} g(\mathbf{x}_{ij})\).

For example, \(\hat{g}_{i} = \textrm{median} \{ g(\mathbf{x}_{i1}), \ldots, g(\mathbf{x}_{in_{i}}) \}\).

For example, \(\hat{g}_{i} = \max\{ g(\mathbf{x}_{i1}), \ldots, g(\mathbf{x}_{in_{i}}) \}\).

To “validate” a risk score, you generally want to look at out-of-sample performance of the risk score.

For example, you might build your risk model using data from individuals enrolled within a specific six-month time window and look at the AUC statistic for outcomes for individuals who enrolled in a different time window.

Looking at the out-of-sample performance over a different time window or using data from a different source is often a good way of justifying the robustness/generalizability of a particular risk model.