Chapter 10 Bootstrap Examples and the Jackknife

10.1 The Parametric Bootstrap for an AR(1) model

Consider the time series \(X_{1}, X_{2}, \ldots, X_{m}\). Here, \(X_{t}\) denotes an observation made at time \(t\).

An autoregressive model of order 1 (usually called an AR(1) model) for this time series is \[\begin{eqnarray} X_{1} &=& \frac{c_{0}}{1 - \alpha} + \varepsilon_{1} \nonumber \\ X_{t} &=& c_{0} + \alpha X_{t-1} + \varepsilon_{t}, \qquad t=2,\ldots,m. \nonumber \end{eqnarray}\]

It is usually assumed that \(|\alpha| < 1\).

In the AR(1) model, it is assumed that

- \(E(\varepsilon_{t}) = 0\)

- \(\textrm{Var}(\varepsilon_{t}) = \sigma^{2}\),

- \(\varepsilon_{2}, \ldots, \varepsilon_{m}\) are i.i.d.

- \(\varepsilon_{t}\) and \(X_{t-1}\) are independent.

In addition to these assumptions, we will assume that \[\begin{equation} \varepsilon_{t} \sim \textrm{Normal}(0, \sigma^{2}) \nonumber \end{equation}\]

The AR(1) model implies that \[\begin{equation} \textrm{Corr}(X_{t}, X_{t-1}) = \alpha \nonumber \end{equation}\] and, more generally, that \[\begin{equation} \textrm{Corr}(X_{t}, X_{t-p}) = \alpha^{p} \nonumber \end{equation}\]

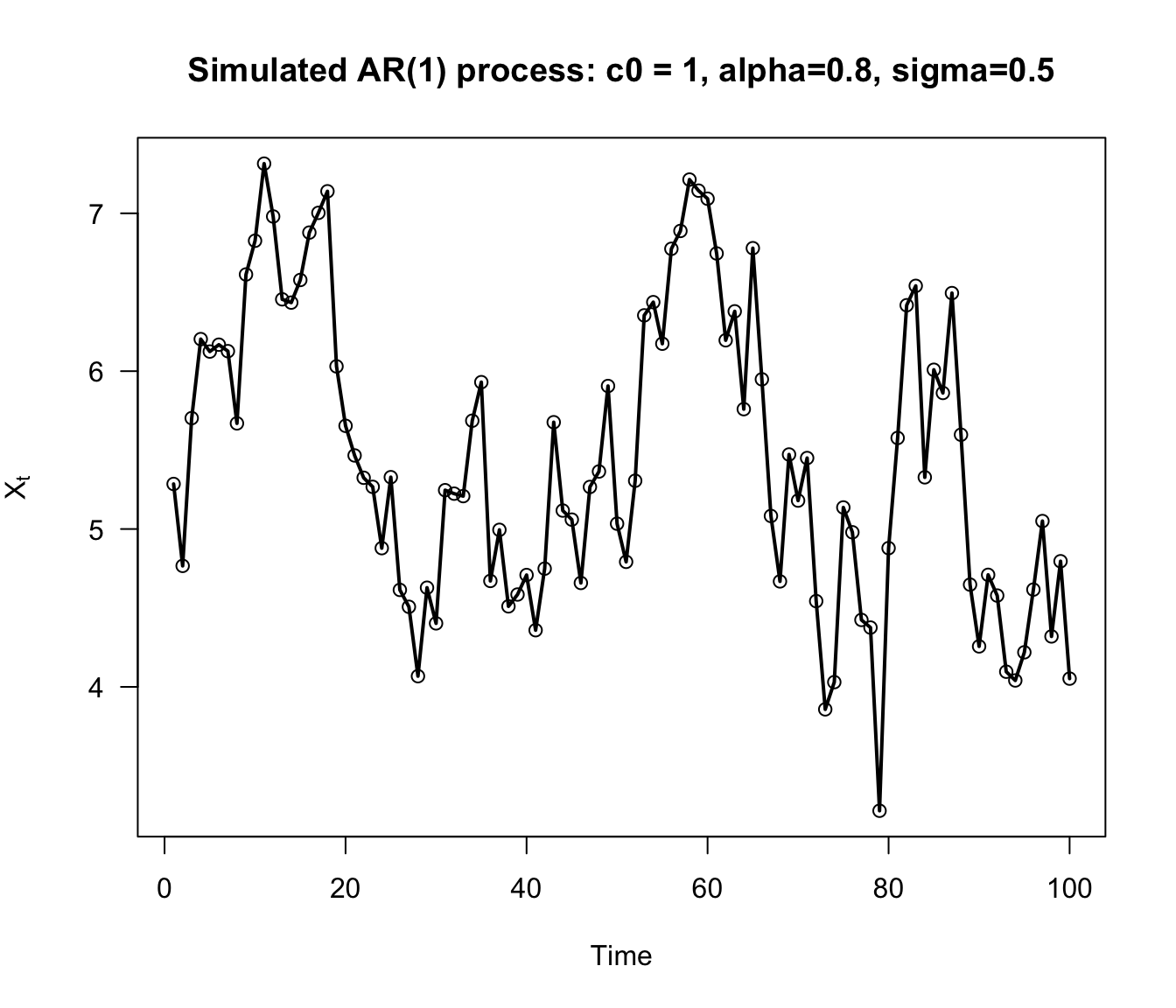

- For known values of \(c_{0}, \alpha\), and \(\sigma^{2}\), we can simulate

an AR(1) time series with the following

Rcode:

SimulateParAR1 <- function(m, c0, alpha, sig.sq) {

xx <- numeric(m)

xx[1] <- c0/(1 - alpha) + rnorm(1, sd=sqrt(sig.sq))

for(t in 2:m) {

xx[t] <- c0 + alpha*xx[t-1] + rnorm(1, sd=sqrt(sig.sq))

}

return(xx)

}

- In

R, estimates of \(c_{0}, \alpha,\) and \(\sigma^{2}\) can be found by using thearfunction. For example,

x <- SimulateParAR1(1000, 1, 0.8, sig.sq=.25)

ar1.fit <- ar(x, aic=FALSE, order.max = 1, method="mle")

c0.est <- ar1.fit$x.mean*(1 - ar1.fit$ar)

alpha.est <- ar1.fit$ar

sigsq.est <- ar1.fit$var.predSuppose we want to construct confidence intervals for \(\alpha\) and \(\sigma\) using a bootstrap method.

Using the direct, nonparametric bootstrap described in the previous chapter will not work because our observations are not independent. There are “block bootstraps” that are designed to work for time series, but we will not discuss those here (see e.g., Bühlmann (2002) or Chapter 8 of Davison and Hinkley (1997) for more details).

With the parametric bootstrap, we only have to use the following steps to generate bootstrap replications \(\hat{\alpha}_{r}^{*}\) and \(\hat{\sigma}_{r}^{2,*}\) for estimates of \(\alpha\) and \(\hat{\sigma}^{2}\).

For \(r = 1, \ldots, R\):

- Simulate a time series \(X_{1}^{*}, \ldots, X_{m}^{*}\) from an AR(1) model with parameters \((\hat{c}_{0}, \hat{\alpha}, \hat{\sigma}^{2})\).

- Compute \(\hat{\alpha}_{r}^{*} = \hat{\alpha}(X_{1}^{*}, \ldots, X_{m}^{*})\).

- Compute \(\hat{\sigma}_{r}^{2,*} = \hat{\sigma}^{2}(X_{1}^{*}, \ldots, X_{m}^{*})\)

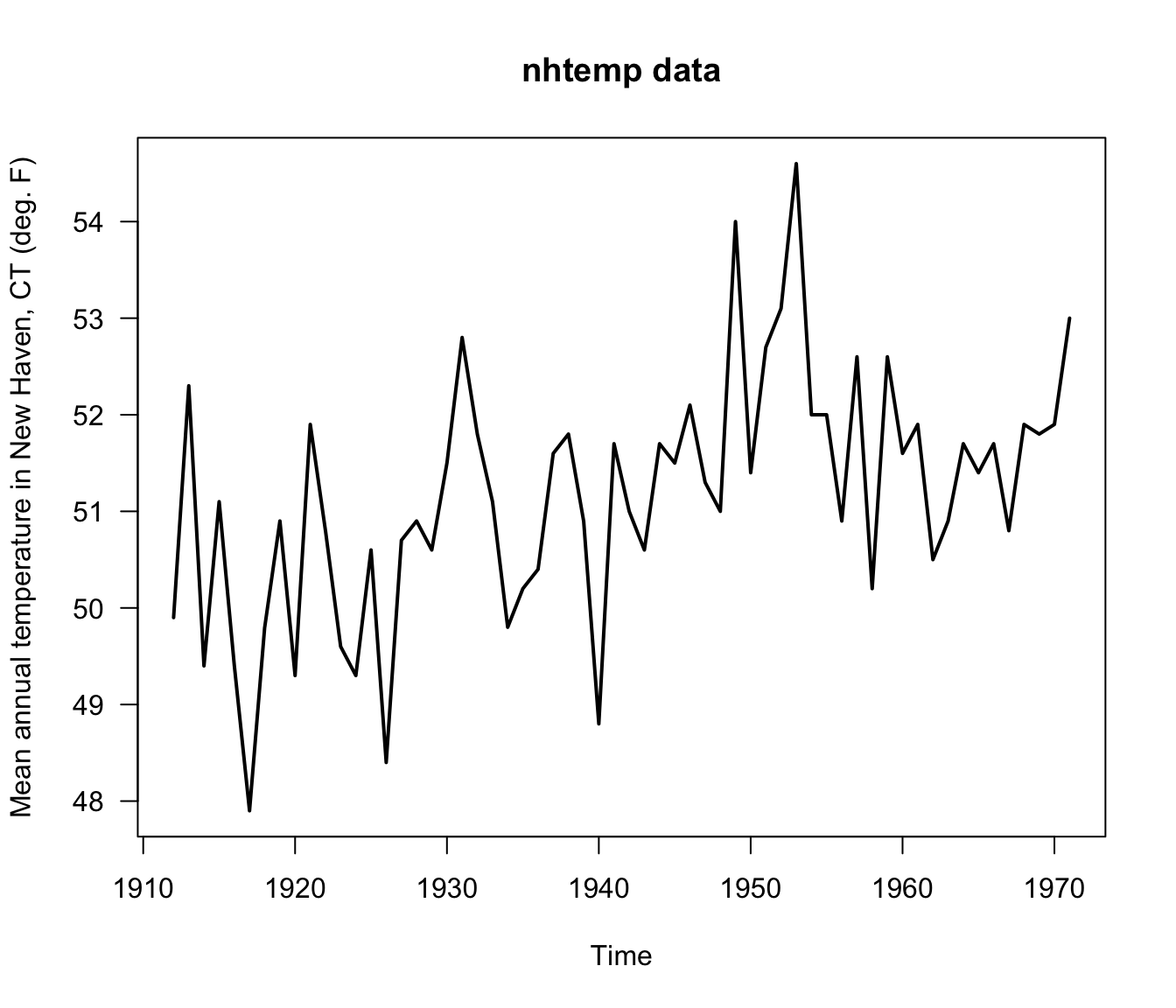

- To see how this parametric bootstrap works, we will use the

nhtempdataset that is available inR.

- The

nhtempdataset contains the mean annual temperature in New Haven, Connecticut from the years 1912-1971

## Time Series:

## Start = 1912

## End = 1917

## Frequency = 1

## [1] 49.9 52.3 49.4 51.1 49.4 47.9- The estimated autocorrelation parameter \(\alpha\) is about \(0.31\) for this data

ar1.temp <- ar(nhtemp, aic=FALSE, order.max = 1)

c0.hat <- ar1.temp$x.mean*(1 - ar1.temp$ar)

alpha.hat <- ar1.temp$ar

sigsq.hat <- ar1.temp$var.pred

alpha.hat## [1] 0.3148269- Now, that we have estimated all the parameter of the AR(1) model, we can run our parametric bootstrap for \(\hat{\alpha}\) and \(\hat{\sigma}\):

R <- 500

alpha.boot <- numeric(R)

sigsq.boot <- numeric(R)

for(r in 1:R) {

x <- SimulateParAR1(60, c0=c0.hat, alpha=alpha.hat, sig.sq=sigsq.hat)

ar1.fit <- ar(x, aic=FALSE, order.max = 1)

alpha.boot[r] <- ar1.fit$ar

sigsq.boot[r] <- ar1.fit$var.pred

}- Normal bootstrap standard error confidence intervals for \(\alpha\) and \(\sigma^{2}\) are

## [1] 0.074 0.556## [1] 0.919 2.017- We can compare our confidence interval for \(\alpha\) with the confidence interval obtained from using a large-sample approximation:

asymp.se <- sqrt(ar1.temp$asy.var.coef)

round(c(alpha.hat - 1.96*asymp.se, alpha.hat + 1.96*asymp.se), 3)## [1] 0.071 0.55910.2 Using the Bootstrap in Regression

In linear regression with a single, univariate covariate, we work with the following model \[\begin{equation} Y_{i} = \beta_{0} + \beta_{1}x_{i} + \varepsilon_{i}, \qquad i = 1, \ldots, n. \nonumber \end{equation}\]

- \(Y_{i}\) - the responses

- \(x_{i}\) - the covariates

- \(\beta_{0}, \beta_{1}\) - the regression coefficients

- \(\varepsilon_{i}\) - the residuals

Typically, confidence intervals for the regression coefficients \(\beta_{0}\) and \(\beta_{1}\) are constructed under the assumption that \(\varepsilon_{i} \sim \textrm{Normal}(0, \sigma^{2})\).

The bootstrap allows us to compute confidence intervals for \((\beta_{0}, \beta_{1})\) without relying on this normality assumption.

How to compute bootstrap confidence intervals for \(\beta_{0}\) and \(\beta_{1}\)?

The least-squares estimates of \(\beta_{0}\) and \(\beta_{1}\) are \[\begin{equation} \hat{\beta}_{0} = \bar{y} - \hat{\beta}_{1}\bar{x} \qquad \qquad \hat{\beta}_{1} = \frac{\sum_{i=1}^{n}(x_{i} - \bar{x})(y_{i} - \bar{y})}{S_{xx}} \nonumber \end{equation}\] where \(S_{xx} = \sum_{i=1}^{n}( x_{i} - \bar{x})^{2}\).

Assuming the covariates are fixed design points, the variance of \(\hat{\beta}_{0}\) and \(\hat{\beta}_{1}\) are \[\begin{equation} \textrm{Var}(\hat{\beta}_{0}) = \sigma^{2}\Big(\frac{\tfrac{1}{n}\sum_{i=1}^{n} x_{i}^{2}}{S_{xx}} \Big) \qquad \textrm{Var}(\hat{\beta}_{1}) = \frac{\sigma^{2}}{S_{xx}} \tag{10.1} \end{equation}\]

10.2.1 Parametric Bootstrap for Regression

With a parametric bootstrap, we will simulate outcomes \(Y_{i}\) from the model \[\begin{equation} Y_{i} = \hat{\beta}_{0} + \hat{\beta}_{1}x_{i} + \varepsilon_{i}, \nonumber \end{equation}\]

- \(\hat{\beta}_{0}\) and \(\hat{\beta}_{1}\) are the least-squares estimates of \(\beta_{0}\) and \(\beta_{1}\),

- \(\varepsilon_{1}, \ldots, \varepsilon_{n}\) are i.i.d. random variables with mean zero and variance \(\hat{\sigma}^{2}\).

It is most common to assume that \(\varepsilon_{i} \sim \textrm{Normal}(0, \hat{\sigma}^{2})\), where \(\hat{\sigma}^{2}\) is an estimate of the residual variance.

However, we could easily use an alternative parametric model for \(\varepsilon_{i}\) if we thought it was appropriate.

A t-distribution with a small number of degrees of freedom can be useful when the residuals are thought to follow a distribution with “heavier tails”.

If we assume \(\varepsilon_{i} \sim \sigma \times t_{3}\), then \(\textrm{Var}(\varepsilon_{i}) = 3\sigma^{2}\).

So, with a \(t_{3}\) residual distribution we want to simulate from the model \[\begin{equation} Y_{i} = \hat{\beta}_{0} + \hat{\beta}_{1}x_{i} + \frac{\hat{\sigma}}{\sqrt{3}}u_{i}, \qquad u_{i} \sim t_{3}, \nonumber \end{equation}\] where \(\hat{\sigma}^{2}\) is the following estimate of the residual variance: \[\begin{equation} \hat{\sigma}^{2} = \frac{1}{n-2}\sum_{i=1}^{n} (Y_{i} - \hat{\beta}_{0} - \hat{\beta}_{1}x_{i})^{2} \nonumber \end{equation}\]

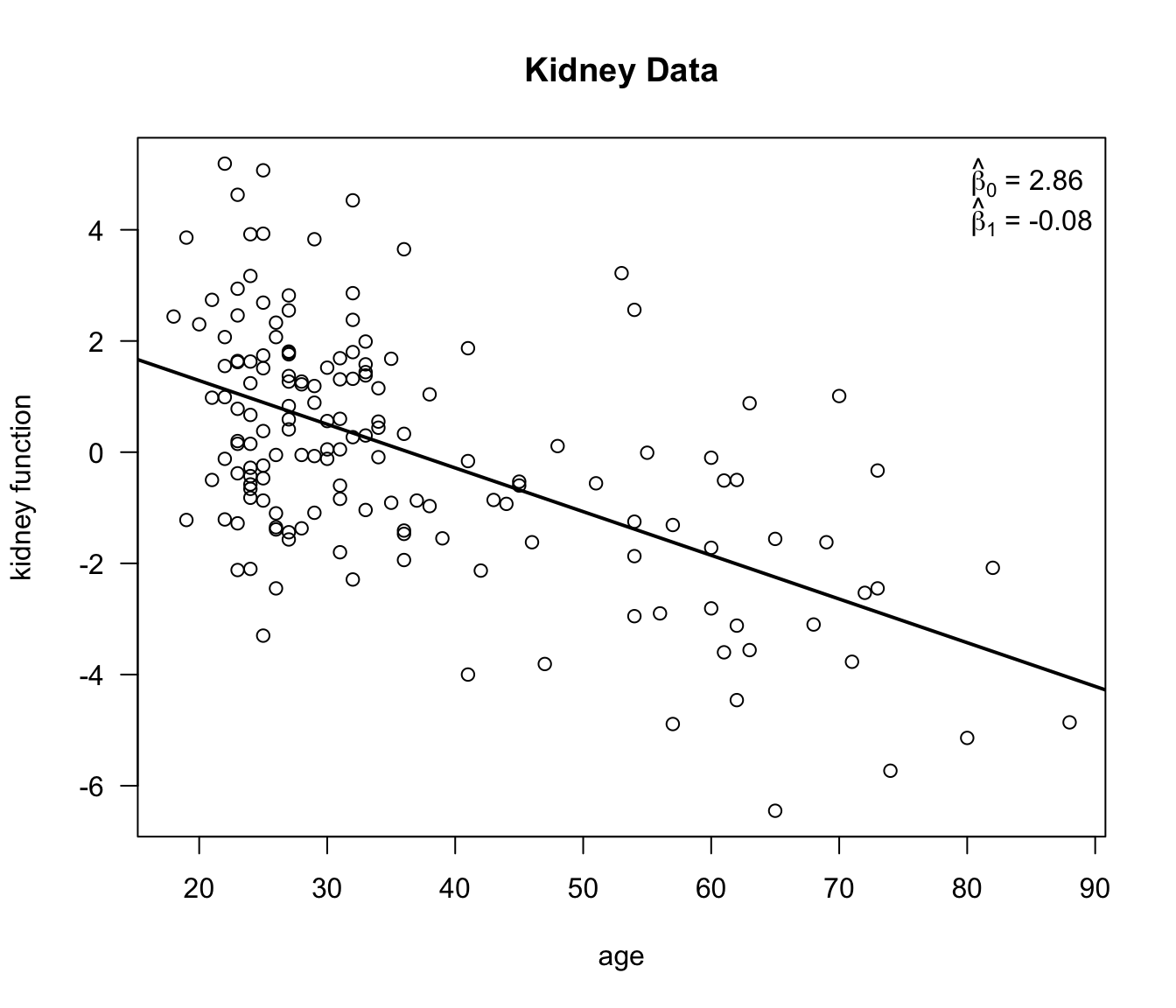

To show how this parametric t-bootstrap works in practice we will look at the kidney function data.

We will look at a linear regression where the measure of kidney function is the outcome and age is the covariate.

- Bootstrap replications of \(\hat{\beta}_{0}\) and \(\hat{\beta}_{1}\) can

be computed using the following

Rcode:

## First find the parameter estimates

lm.kidney <- lm(tot ~ age, data=kidney)

beta0.hat <- lm.kidney$coef[1]

beta1.hat <- lm.kidney$coef[2]

sigsq.hat <- sum(lm.kidney$residuals^2)/(157 - 2)

## Using these estimates, run a parametric bootstrap to generate

## bootstrap replications of beta0.hat and beta1.hat

R <- 500

beta0.boot <- numeric(R)

beta1.boot <- numeric(R)

se.beta0.boot <- numeric(R)

se.beta1.boot <- numeric(R)

for(r in 1:R) {

ysim <- beta0.hat + beta1.hat*kidney$age + sqrt(sigsq.hat/3)*rt(157, df=3)

lm.boot <- lm(ysim ~ kidney$age)

beta0.boot[r] <- lm.boot$coef[1]

beta1.boot[r] <- lm.boot$coef[2]

## This code can be used to find the standard errors from this bootstrap sample

sig.hatr <- summary(lm.boot)$sigma

se.beta0.boot[r] <- sig.hatr*sqrt(summary(lm.boot)$cov.unscaled[1,1])

se.beta1.boot[r] <- sig.hatr*sqrt(summary(lm.boot)$cov.unscaled[2,2])

}Because we have the formulas for the standard errors of \(\beta_{0}\) and \(\beta_{1}\), we can use studentized bootstrap confidence intervals without using the double bootstrap approach.

Estimates of the standard error for the \(r^{th}\) bootstrap replication are \[\begin{eqnarray} \hat{se}_{r}(\beta_{0}) &=& \hat{\sigma}_{r}\sqrt{\frac{\tfrac{1}{n}\sum_{i=1}^{n} x_{i}^{2}}{S_{xx}}} \nonumber \\ \hat{se}_{r}(\beta_{1}) &=& \hat{\sigma}_{r}/\sqrt{S_{xx}} \end{eqnarray}\]

These standard error estimates come from applying the formulas in (10.1) to the \(r^{th}\) bootstrap sample.

Recall from Chapter 9 that the studentized confidence intervals are found by using the following formula. \[\begin{equation} \Big[ T_{n} - se_{boot} \times \hat{K}_{R}^{-1}(1 - \alpha/2), T_{n} - se_{boot} \times \hat{K}_{R}^{-1}(\alpha/2) \Big] \nonumber \end{equation}\]

Rcode to compute the studentized confidence intervals is given below:

## First get estimates of the standard error of our estimates

## I use the formulas for the regression standard errors, but

## we could have used a bootstrap estimate.

se.est0 <- summary(lm.kidney)$sigma*sqrt(summary(lm.boot)$cov.unscaled[1,1])

se.est1 <- summary(lm.kidney)$sigma*sqrt(summary(lm.boot)$cov.unscaled[2,2])

stu.quants0 <- quantile( (beta0.boot - beta0.hat)/se.beta0.boot, probs=c(0.025, 0.975))

stu.quants1 <- quantile( (beta1.boot - beta1.hat)/se.beta1.boot, probs=c(0.025, 0.975))- The studentized bootstrap confidence intervals are then

## Confidence interval for beta0

c(beta0.hat - stu.quants0[2]*se.est0, beta0.hat - stu.quants0[1]*se.est0)## (Intercept) (Intercept)

## 2.11 3.51## Confidence interval for beta1

c(beta1.hat - stu.quants1[2]*se.est1, beta1.hat - stu.quants1[1]*se.est1)## age age

## -0.0954 -0.0608- Compare these studentized bootstrap confidence intervals with the confidence intervals computed under the normality assumption for the residuals:

## 2.5 % 97.5 %

## (Intercept) 2.1497 3.5703

## age -0.0965 -0.060710.2.2 Nonparametric Bootstrap for Regression

If we think of the \(x_{i}\) as fixed values, the \(Y_{i}\) in a linear regression are not i.i.d. because the means are not the same.

This suggests that we cannot use the usual nonparametric bootstrap to construct confidence intervals for \(\beta_{0}\) and \(\beta_{1}\).

However, if we also view the \(x_{i}\) as random, we can view the pairs of observations \((Y_{1}, x_{1}), \ldots, (Y_{n}, x_{n})\) as i.i.d. observations from a bivariate distribution.

In this case, you can also think of \(\hat{\beta}_{1}\) as an estimate of the following quantity \[\begin{equation} \rho_{YX}\frac{\sigma_{y}}{\sigma_{x}} \nonumber \end{equation}\] where \(\rho_{YX} = \textrm{Corr}(Y_{i}, x_{i})\).

In the case when \((Y_{i}, x_{i})\) are bivariate normal, the conditional expectation of \(Y_{i}\) given \(x_{i}\) has the linear regression structure: \[\begin{equation} E(Y_{i}| x_{i}) = \beta_{0} + \beta_{1}x_{i}, \nonumber \end{equation}\] where \(\beta_{0} = \mu_{y} - \rho_{YX}\frac{\sigma_{y}\mu_{x}}{\sigma_{x}}\) and \(\beta_{1} = \rho_{YX}\frac{\sigma_{y}}{\sigma_{x}}\).

So, even if the linear model is not exactly true, our estimate and confidence interval still has a clear interpretation.

If the linear model assumption is true, the true standard error of \(\hat{\beta}_{0}\) and \(\hat{\beta}_{1}\) will be slightly different than the formulas shown in (10.1). Nevertheless, (10.1) can be thought of as consistent estimates of the true standard error.

If we are thinking of the observations \((Y_{1}, x_{1}), \ldots, (Y_{n}, x_{n})\) as i.i.d. pairs, we can use the nonparametric bootstrap by just subsampling pairs of observations.

So, to generate bootstrap replications \(\hat{\beta}_{0,r}^{*}\), \(\hat{\beta}_{1, r}^{*}\) for \(\hat{\beta}_{0}\) and \(\hat{\beta}_{1}\), we just use the following procedure

For \(r = 1, \ldots, R\):

- Draw a sample of size \(n\): \(\big((Y_{1}^{*}, x_{1}^{*}), \ldots, (Y_{n}^{*}, x_{n}^{*}) \big)\) by sampling with replacement from the original data.

- Compute \(\hat{\beta}_{0,r}^{*}\) and \(\hat{\beta}_{1,r}^{*}\) from this bootstrap sample.

Rcode for generating these bootstrap replications for thekidneydata is below:

R <- 500

beta0.boot.np <- numeric(R)

beta1.boot.np <- numeric(R)

se.beta0.boot.np <- numeric(R)

se.beta1.boot.np <- numeric(R)

for(r in 1:R) {

subsamp.ind <- sample(1:157, size=157, replace=TRUE)

kidney.tmp <- kidney[subsamp.ind,]

lm.boot <- lm(tot ~ age, data=kidney.tmp)

beta0.boot.np[r] <- lm.boot$coef[1]

beta1.boot.np[r] <- lm.boot$coef[2]

## This code can be used to find the standard errors from this bootstrap sample

sig.hatr <- summary(lm.boot)$sigma

se.beta0.boot.np[r] <- sig.hatr*sqrt(summary(lm.boot)$cov.unscaled[1,1])

se.beta1.boot.np[r] <- sig.hatr*sqrt(summary(lm.boot)$cov.unscaled[2,2])

}- To find the studentized confidence intervals for this nonparametric bootstrap, we can use the following code:

se.est0 <- summary(lm.kidney)$sigma*sqrt(summary(lm.boot)$cov.unscaled[1,1])

se.est1 <- summary(lm.kidney)$sigma*sqrt(summary(lm.boot)$cov.unscaled[2,2])

stu.quants0.np <- quantile( (beta0.boot.np - beta0.hat)/se.beta0.boot.np,

probs=c(0.025, 0.975))

stu.quants1.np <- quantile( (beta1.boot.np - beta1.hat)/se.beta1.boot.np,

probs=c(0.025, 0.975))- The studentized bootstrap confidence intervals for \(\beta_{0}\) and \(\beta_{1}\) are then

## Confidence interval for beta0

c(beta0.hat - stu.quants0.np[2]*se.est0, beta0.hat - stu.quants0.np[1]*se.est0)## (Intercept) (Intercept)

## 2.16 3.68## Confidence interval for beta1

c(beta1.hat - stu.quants1.np[2]*se.est1, beta1.hat - stu.quants1.np[1]*se.est1)## age age

## -0.1006 -0.0596Regression with more than 1 covariate

If we have more than one covariate in our model, for example, \[\begin{equation} Y_{i} = \beta_{0} + \beta_{1}x_{i1} + \ldots + \beta_{p}x_{ip} + \varepsilon_{i}, \nonumber \end{equation}\] the bootstrap works essentially the same as for the case with a single covariate.

For the parametric bootstrap with a Normal residual distribution, you would just simulate \(Y_{i}^{*} \sim \textrm{Normal}(\hat{\beta}_{0} + \hat{\beta}_{1}x_{i1} + \ldots + \hat{\beta}_{p}x_{ip}, \hat{\sigma}^{2})\).

For the nonparametric bootstrap, you would subsample pairs \((Y_{1}^{*}, x_{1}^{*}), \ldots, (Y_{n}^{*}, x_{n}^{*})\) as described before, and compute your regression coefficients \(\hat{\beta}_{0,r}^{*}, \hat{\beta}_{1,r}^{*}, \ldots, \hat{\beta}_{p,r}^{*}\) from this bootstrap sample.

10.3 Pointwise Confidence Intervals for a Density Function

Recall that a kernel density estimate of an unknown probability density \(f(x)\) has the form \[\begin{equation} \hat{f}_{h_{n}}(x) = \frac{1}{n h_{n}}\sum_{i=1}^{n} K\Big( \frac{x - X_{i}}{h_{n}} \Big) \nonumber \end{equation}\]

We cannot naively apply the Central Limit Theorem, because \(h_{n}\) is changing as \(n \longrightarrow \infty\).

Nevertheless, you can show (see, e.g., Tsybakov (2008)) that \[\begin{equation} \sqrt{nh_{n}}\Big( \hat{f}_{h_{n}}(x) - E\{ \hat{f}_{h_{n}}(x) \} \Big) \longrightarrow \textrm{Normal}\big( 0, \kappa_{2}(K) f(x) \big) \nonumber \end{equation}\] provided that \(h_{n} \longrightarrow 0\) and \(nh_{n} \longrightarrow \infty\). Here, \(\kappa_{2}(K) = \int_{-\infty}^{\infty} K^{2}(u) du\).

This suggests that a standard error estimate for \(\hat{f}_{h_{n}}(x)\) is \(\sqrt{\kappa_{2}(K)\hat{f}_{h_{n}}(x)/nh_{n}}\) and a \(95\%\) confidence interval for \(E\{ \hat{f}_{h_{n}}(x) \}\) is \[\begin{equation} \Bigg[ \hat{f}_{h_{n}}(x) - 1.96 \times \sqrt{\frac{\kappa_{2}(K) \hat{f}_{h_{n}}(x) }{nh_{n}}}, \hat{f}_{h_{n}}(x) + 1.96 \times \sqrt{\frac{\kappa_{2}(K) \hat{f}_{h_{n}}(x)}{nh_{n}}} \Bigg] \nonumber \end{equation}\]

Notice that this is a confidence interval for \(E\{ \hat{f}_{h_{n}}(x) \}\) rather than \(f(x)\).

So, you can roughly think of this as a confidence interval for a smoothed version of \(f(x)\) at \(x\): \[\begin{equation} E\{ \hat{f}_{h_{n}}(x) \} = \frac{1}{h_{n}}\int_{-\infty}^{\infty} K\Big( \frac{x - t}{h_{n}} \Big) f(t) dt \nonumber \end{equation}\]

Notice also that this is a pointwise confidence interval. It is not a confidence band.

Methods for computing “bias-corrected” confidence intervals for \(f(x)\) are discussed, for example, in Chen (2017).

To get a bootstrap estimate of the standard deviation of \(\hat{f}_{h_{n}}(x)\), we can use the usual steps.

For \(r=1, \ldots, R\):

- Draw a sample of size \(n\): \((X_{1}^{*}, \ldots, X_{n}^{*})\) by sampling with replacement from \(\mathbf{X}\).

- Compute \(T_{n,r}^{*} = \tfrac{1}{nh_{n}}\sum_{i=1}^{n} K(\tfrac{x - X_{i}^{*}}{ h_{n} } )\).

Then, compute the estimated standard error: \[\begin{equation} \hat{se}_{boot} = \Big[ \frac{1}{R-1} \sum_{r=1}^{R} \Big( T_{n,r}^{*} - \frac{1}{R} \sum_{r=1}^{R} T_{n,r}^{*} )^{2} \Big]^{1/2} \end{equation}\]

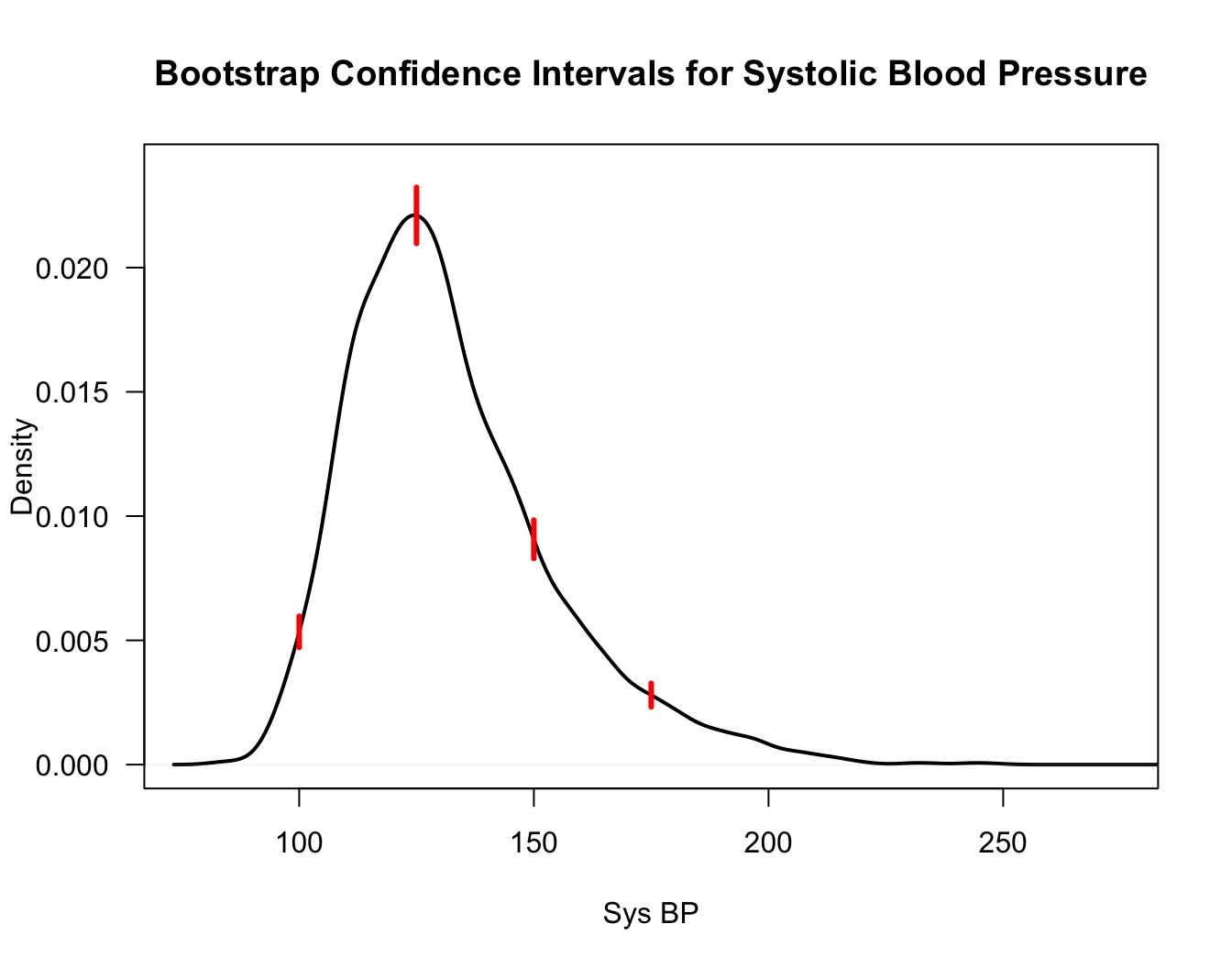

Rcode to compute these standard error estimates for thesysBPvariable from theframinghamdataset is given below

framingham <- read.csv("~/Library/Mobile Documents/com~apple~CloudDocs/Documents/STAT685Notes/Data/framingham.csv")

R <- 500

BootMat <- matrix(0, nrow=R, ncol=4)

for(r in 1:R) {

xx.boot <- sample(framingham$sysBP, size=length(framingham$sysBP), replace=TRUE)

kk.boot <- density(xx.boot)

tmp <- approxfun(kk.boot$x, kk.boot$y)

BootMat[r,] <- c(tmp(100), tmp(125), tmp(150), tmp(175))

}

bb <- apply(BootMat, 2, sd)

Figure 10.1: Bootstrap confidence intervals for the density function at the points x=100, 125, 150, 175

10.4 When can the Bootstrap Fail?

While the bootstrap is very automatic and could be used to construct confidence intervals in nearly any situation, these bootstrap confidence intervals may fail to give the correct coverage in some situations.

A few situations in which the bootstrap can fail include:

- If we are interested in estimating a parameter \(\theta\) and the support \(\{ x: f_{\theta}(x) > 0\}\) of the density function depends on \(\theta\).

- If there are parameter constraints and the true value of the parameter lies on the boundary of the parameter space. For example, we estimate \(\theta\) subject to the constraint that \(\theta \geq 0\), and the true value of \(\theta\) is zero.

- If \(T_{n} = g(\bar{X})\) and \(g'(\mu) = 0\) where \(\mu = E(X_{1})\).

- No finite mean. If \(E(|X_{1}|)\) is not finite, then the bootstrap may not work well.

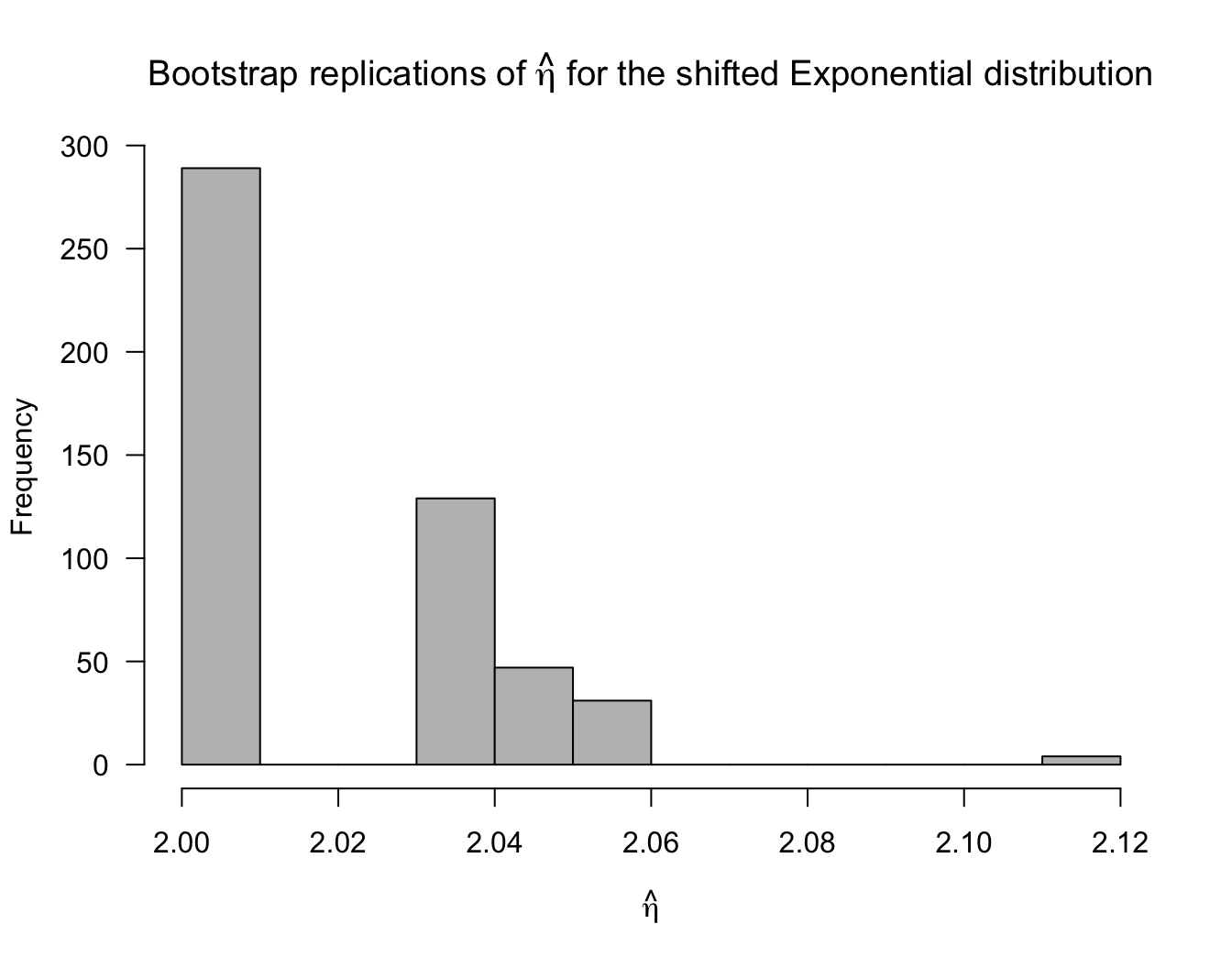

10.4.1 Example: The Shifted Exponential Distribution

Let us consider observations \(X_{1}, \ldots, X_{n}\) that follow the shifted exponential distribution whose density function is \[\begin{equation} f(x) = \begin{cases} \lambda e^{-\lambda(x - \eta)} & \textrm{ if } x \geq \eta \nonumber \\ 0 & \textrm{otherwise} \nonumber \end{cases} \end{equation}\] where \(\lambda > 0\) and \(\eta > 0\).

The maximum likelihood estimates of \(\lambda\) and \(\eta\) are \[\begin{equation} \hat{\lambda} = \frac{1}{\bar{X}} - X_{(1)} \qquad \hat{\eta} = X_{(1)} \nonumber \end{equation}\] where \(X_{(1)} = \min\{ X_{1}, \ldots, X_{n} \}\) is the smallest observation.

Notice that this is an example where the support of the density function depends on the parameter \(\eta\).

Suppose we use the bootstrap to construct confidence intervals for \(\lambda\) and \(\eta\). What will happen?

Let us consider an example where we have i.i.d. data \(X_{1}, \ldots, X_{n}\) that follow a shifted Exponential distribution with \(\lambda = 1/3\) and \(\eta = 2\).

The following code can estimate the coverage proportion of a bootstrap confidence interval for \(\eta\):

n <- 200

R <- 500

eta.true <- 2

nreps <- 500

Cover.bootsd.ci <- numeric(nreps)

for(k in 1:nreps) {

## Step 1: Generate the Data and compute the estimate of eta

xx <- 2 + rexp(n, rate=1/3)

eta.hat <- min(xx)

## Step 2: Find bootstrap confidence intervals using R bootstrap replications

eta.boot <- numeric(R)

for(r in 1:R) {

boot.xx <- sample(xx, size=n, replace = TRUE)

eta.boot[r] <- min(boot.xx)

}

boot.ci.sd <- c(eta.hat - 1.96*sd(eta.boot), eta.hat + 1.96*sd(eta.boot))

## Step 3: Record if the true parameter is covered or not:

Cover.bootsd.ci[k] <- ifelse(boot.ci.sd[1] < eta.true & boot.ci.sd[2] >= eta.true,

1, 0)

}- The estimated coverage for this bootstrap confidence interval is

## [1] 0.8

10.5 The Jackknife

The jackknife is also a nonparametric method for estimating standard errors.

Like the bootstrap, the jackknife also uses the idea of looking at multiple subsets of the data.

Also like the bootstrap, the jackknife is completely automatic in the sense that we only need to be able to compute our statistic of interest, and we do not need to do any formal calculations to find the standard error.

While the jackknife was actually developed before the bootstrap, it is used much less than the bootstrap is in applications - at least in the context of finding confidence intervals.

We will define \(\mathbf{X}_{-i}\) to be the vector of observations that has the \(i^{th}\) observation deleted: \[\begin{equation} \mathbf{X}_{(-i)} = (X_{1}, \ldots, X_{i-1}, X_{i+1}, \ldots, X_{n}) \nonumber \end{equation}\]

Define \(T_{n,(-i)}\) to be the value of the statistic \(T_{n}\) when using data which has the \(i^{th}\) observation removed \[\begin{equation} T_{n, (-i)} = h(X_{1}, \ldots, X_{i-1}, X_{i+1}, \ldots, X_{n}) \nonumber \end{equation}\]

The jackknife estimate of the standard error of \(T_{n}\) is \[\begin{equation} \hat{se}_{jack} = \Big[ \frac{n-1}{n} \sum_{i=1}^{n} ( T_{n, (-i)} - \bar{T}_{n, jack} )^{2} \Big]^{1/2}, \nonumber \end{equation}\] where \(\bar{T}_{n,jack} = \tfrac{1}{n} \sum_{i=1}^{n} T_{n, (-i)}\).

An advantage of the jackknife is that, like the bootstrap, it does not make any particular parametric assumptions about the distribution of the data.

However, the jackknife is more dependent on a smoothness assumption (that is smoothness across slightly perturbed datasets) than the bootstrap. An example of this is the sample median where, if we delete one observation, the sample median has a different definition due to the sample size being even vs. odd.

10.6 Exercises

Exercise 10.1 Using the parametric bootstrap, compute studentized bootstrap confidence intervals for \(\beta_{0}\) and \(\beta_{1}\) in the

kidneydata example. This time, assume that \(\varepsilon_{i} \sim \textrm{Normal}(0, \hat{\sigma}^{2})\).Exercise 10.2 Another way of using the bootstrap in a regression context is to resample the residuals from the fitted regression model. Speficially, we first fit the linear regression model and compute residuals \(\hat{e}_{1}, \ldots, \hat{e}_{n}\) via \[\begin{equation} \hat{e}_{i} = Y_{i} - \hat{\beta}_{0} - \hat{\beta}_{1}x_{i} \nonumber \end{equation}\] One then generates a bootstrap sample by first subsampling \((\hat{e}_{1}^{*}, \ldots, \hat{e}_{n}^{*})\) from the vector of “original” residuals \((\hat{e}_{1}, \ldots, \hat{e}_{n})\) and then setting \(Y_{i}^{*} = \hat{\beta}_{0} + \hat{\beta}_{1}x_{i} + \hat{e}_{i}^{*}\). You then compute the bootstrap replications \(\hat{\beta}_{0,r}^{*}\) and \(\hat{\beta}_{1,r}^{*}\) by fitting a linear regression with data: \((Y_{1}^{*}, x_{1}), \ldots, (Y_{n}^{*}, x_{n})\).

Using the kidney data, try using this procedure to construct \(95\%\) bootstrap confidence intervals

for \(\beta_{0}\) and \(\beta_{1}\).